- English

- Farsi | فارسی

- Pashto | پشثو

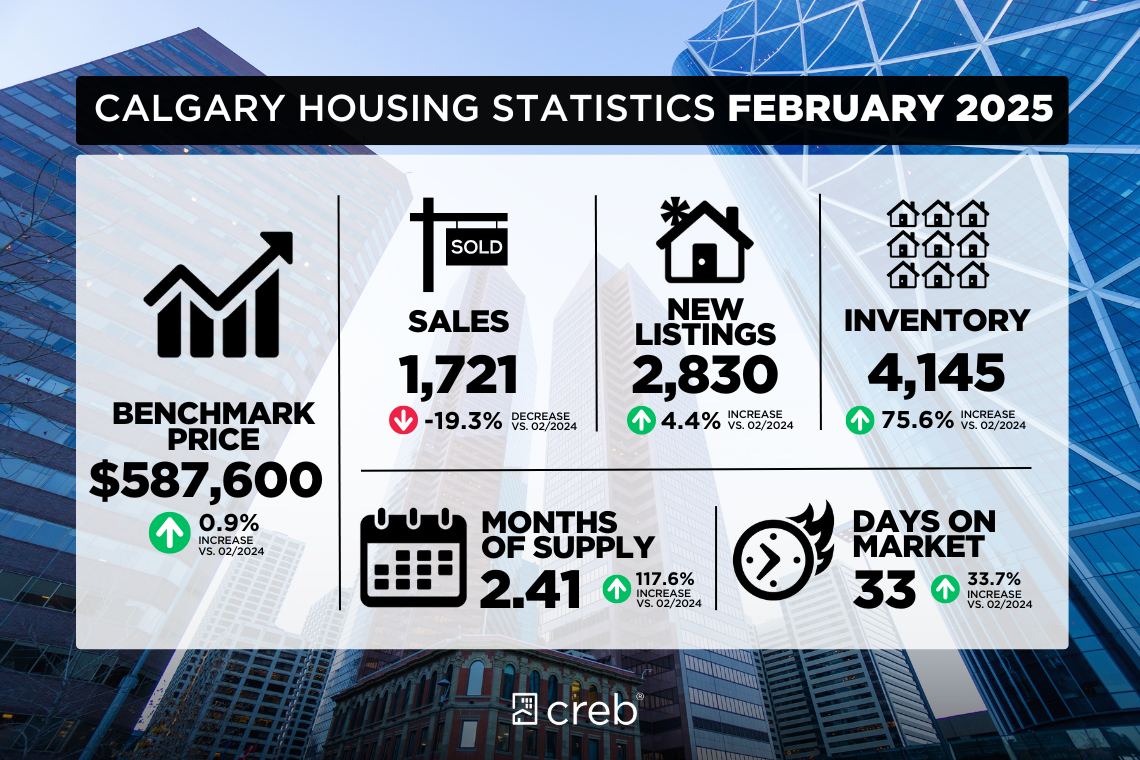

Inventory levels saw substantial year-over-year growth for the second month in a row, rising by 76 per cent to 4,145 units in February. While inventory increases were seen across all price ranges, the largest increases were in homes priced under $500,000.

The increase was driven by substantial growth in the more affordable apartment and row/townhouse sectors. The overall months of supply was 2.4 in February, similar to last month but more than double this time last year. Apartment-style units remained the most well-supplied at 3.1 months.

There were 1,721 sales in February, which was above historical averages for the month but 19 per cent lower than levels seen last year and significantly lower than the record levels seen in the post-pandemic period. New Listings in February reached 2,830, roughly in line with historical averages for the month. The sales-to-new listings ratio for the month was 61 per cent, higher than historical averages but below levels seen in each of the last three years.

“Even though more people listed their homes for sale, there were actually fewer sales than in February 2024. So, we’re seeing the seller’s market of the past two or three years ease off,” said Alan Tennant, President and CEO of CREB®. “In turn, that’s caused the pace at which prices are increasing to slow down a bit, which should come as welcome news for buyers.”

The total residential unadjusted benchmark price in February was $587,600, relatively stable compared to late-2024 and roughly one per cent higher year-over-year. Price changes varied across the city, with the City Centre and North districts seeing declines, while the East district saw the largest price growth at over three per cent.

Detached

Sales in February slowed to 765 units, nearly 20 per cent lower than last year. New Listings increased by nearly six per cent year-over-year to 1,265 units. The decline in sales, coupled with the gain in new listings, drove inventory levels higher, reaching 1,698 and a 61 per cent increase in levels compared to 2024.

Months of supply improved across all districts compared to the levels seen last year, although the recovery is uneven across the city. The City Centre and North East districts continue to trend towards more balanced conditions, while the South and North West districts remain supply-constrained at approximately 1.6 months.

The unadjusted benchmark price rose to $760,500, roughly five per cent higher than last February. Prices rose across all districts, with the largest increase occurring in the City Centre district at nearly eight per cent growth.

Semi-Detached

There were 240 new listings in February, a gain of seven per cent from 2024. Sales fell by nearly 14 per cent compared to 2024, slowing to 165 units. This gap between sales and new listings drove inventories up by 46 per cent, though they remain below long-term averages for the sector in February. There was a large variation in months of supply across the city, with a low of just one month in the North West district compared to a high of eight months in the East district.

The unadjusted benchmark price pushed above levels seen in the late summer and early fall, rising by nearly seven per cent year-over-year to $683,500. This increase was supported by price grains across all districts, with the largest growth occurring in the City Centre and South districts of approximately eight per cent.

Row

As with other property types, year-over-year sales fell by over nine per cent while new listings increased by almost four per cent. Despite the sales decline, both sales and new listings remain above long-term averages for the month. This drop in sales pushed inventories to 655 units, more than double the levels seen last year, though still lower than the historical average levels for February. Months of supply improved across the city; the South and East districts have the tightest conditions at under 1.5 months, while the North East district has almost three months.

As with other property types, year-over-year sales fell by over nine per cent while new listings increased by almost four per cent. Despite the sales decline, both sales and new listings remain above long-term averages for the month. This drop in sales pushed inventories to 655 units, more than double the levels seen last year, though still lower than the historical average levels for February. Months of supply improved across the city; the South and East districts have the tightest conditions at under 1.5 months, while the North East district has almost three months.

Unadjusted benchmark prices remain below levels seen in the fall but are up almost three per cent year-over-year at $446,880. Prices increased across all districts, with marginal increases in the South East and North districts, while the East district experienced a significant 12 per cent increase compared to 2024.

Apartment Condominium

Sales reached 473 units in February, 26 per cent lower than last year but still well above long-term averages for the apartment sector in February. New listings were relatively flat year-over-year, but at 852 units, it was the highest amount on record for the month. Driven by the record new listings, inventory increased by 90 per cent year-over-year and also pushed to near-record levels. Months of supply reached 3.1 months in February, a substantial 155 per cent increase over 2024 but still well below record levels seen in the period between the 2014 oil crash and the pandemic.

Sales reached 473 units in February, 26 per cent lower than last year but still well above long-term averages for the apartment sector in February. New listings were relatively flat year-over-year, but at 852 units, it was the highest amount on record for the month. Driven by the record new listings, inventory increased by 90 per cent year-over-year and also pushed to near-record levels. Months of supply reached 3.1 months in February, a substantial 155 per cent increase over 2024 but still well below record levels seen in the period between the 2014 oil crash and the pandemic.

The unadjusted benchmark price for February was $334,200, comparable to levels seen in the fall and almost four per cent above the prices seen this time last year. The largest price growth occurred in the West district at over eight per cent.

REGIONAL MARKET FACTS

Airdrie

The overall Airdrie market fell roughly in line with its long-term averages in February, with sales declining while new listings and inventories rose to levels typical of the month. Sales declined by nearly nine per cent, reaching 123 units, while new listings increased by nearly 23 per cent to 225 units. This drop in sales, combined with an increase in new listings, pushed inventories to over double the amount seen last year, rising to 345 homes. As a result, months of supply pushed up to nearly three months, also in line with long-term averages and the highest seen in the market since before the pandemic.

The unadjusted benchmark price for February was essentially flat compared to last month and remained below levels seen in the fall at $537,600, but were 1.6 per cent higher than seen last February.

Cochrane

Sales in February reached 75 units, while new listings reached 126 units, both increases over this time last year and above long-term averages for the market. Inventory increased by over 48 per cent year-over-year to 196 units, the highest level seen in any month since the spring of 2021 but still below long-term averages for February in the Cochrane market. This increase in inventory allowed the months of supply to recover to 2.6 months, the highest since the pandemic but still well below historical levels for the month. The relatively tight conditions supported prices recovering near the record-high levels seen in the summer, as the unadjusted benchmark price increased by over five per cent year-over-year to $577,100.

Sales in February reached 75 units, while new listings reached 126 units, both increases over this time last year and above long-term averages for the market. Inventory increased by over 48 per cent year-over-year to 196 units, the highest level seen in any month since the spring of 2021 but still below long-term averages for February in the Cochrane market. This increase in inventory allowed the months of supply to recover to 2.6 months, the highest since the pandemic but still well below historical levels for the month. The relatively tight conditions supported prices recovering near the record-high levels seen in the summer, as the unadjusted benchmark price increased by over five per cent year-over-year to $577,100.

Okotoks

February saw sales decline by four per cent year-over-year to 45 units, though they remained in line with long-term averages for the month. New listings increased by seven per cent compared to 2024, and, at 60 units, remained well below levels typically seen in February. Inventory recovered to 69 units, 19 per cent above 2024, but as with new listings, they remained significantly lower than historical levels for the month. These tighter inventory levels also kept the months of supply well below what would typically be seen in February at just 1.5 months. Despite the tight conditions, the unadjusted benchmark price for the month was relatively flat compared to January and under one per cent higher than in 2024.

February saw sales decline by four per cent year-over-year to 45 units, though they remained in line with long-term averages for the month. New listings increased by seven per cent compared to 2024, and, at 60 units, remained well below levels typically seen in February. Inventory recovered to 69 units, 19 per cent above 2024, but as with new listings, they remained significantly lower than historical levels for the month. These tighter inventory levels also kept the months of supply well below what would typically be seen in February at just 1.5 months. Despite the tight conditions, the unadjusted benchmark price for the month was relatively flat compared to January and under one per cent higher than in 2024.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.

رشد قابل توجه سطوح موجودی برای دومین ماه متوالی

سطح موجودیها در فوریه برای دومین ماه پیاپی نسبت به سال گذشته رشد قابل توجهی داشت و با افزایش ۷۶ درصدی به ۴,۱۴۵ واحد رسید. در حالی که افزایش موجودی در تمام ردههای قیمتی مشاهده شد، بزرگترین افزایشها در خانههای با قیمت زیر ۵۰۰,۰۰۰ دلار بود.

این افزایش به دلیل رشد قابل توجه در بخشهای مقرونبهصرفهتر آپارتمانها و خانههای ردیفی/تاونهاوس بود. میزان ماههای عرضه کل در فوریه ۲.۴ بود، مشابه ماه گذشته اما بیش از دو برابر نسبت به همین زمان در سال گذشته. واحدهای آپارتمانی با ۳.۱ ماه عرضه، همچنان بیشترین موجودی را داشتند.

در فوریه ۱,۷۲۱ فروش انجام شد که بالاتر از میانگینهای تاریخی برای این ماه بود، اما ۱۹ درصد کمتر از سطح سال گذشته و بهطور قابل توجهی پایینتر از سطوح رکوردی که در دوره پس از همهگیری دیده شده بود. تعداد لیستینگهای جدید در فوریه به ۲,۸۳۰ رسید که تقریباً با میانگینهای تاریخی این ماه همراستا بود. نسبت فروش به لیستینگهای جدید در این ماه ۶۱ درصد بود، که بالاتر از میانگینهای تاریخی است اما کمتر از سطوح مشاهدهشده در هر یک از سه سال گذشته بود.

آلن تنانت، رئیس و مدیرعامل CREB® گفت: «با وجود اینکه افراد بیشتری خانههای خود را برای فروش لیست کردند، فروش واقعی نسبت به فوریه ۲۰۲۴ کمتر بود. بنابراین، ما شاهد کاهش فشار بازار فروشندگان در دو یا سه سال گذشته هستیم. در نتیجه، این باعث شده که سرعت افزایش قیمتها کمی کند شود، که باید خبر خوشایندی برای خریداران باشد.»

قیمت معیار مسکونی بدون تعدیل در فوریه ۵۸۷,۶۰۰ دلار بود، که نسبت به اواخر ۲۰۲۴ تقریباً پایدار و حدود یک درصد بیشتر از سال گذشته است. تغییرات قیمت در سراسر شهر متفاوت بود، به طوری که مناطق مرکزی شهر و شمالی کاهش قیمت داشتند، در حالی که منطقه شرقی با بیش از سه درصد بیشترین رشد قیمت را تجربه کرد.

خانههای مستقل

فروش در فوریه به ۷۶۵ واحد کاهش یافت، که نزدیک به ۲۰ درصد کمتر از سال گذشته است. لیستینگهای جدید با افزایش نزدیک به ۶ درصدی نسبت به سال گذشته به ۱,۲۶۵ واحد رسید. کاهش فروش همراه با افزایش لیستینگهای جدید، سطح موجودی را به ۱,۶۹۸ واحد رساند که نسبت به سال ۲۰۲۴ افزایش ۶۱ درصدی را نشان میدهد.

ماههای عرضه در تمام مناطق نسبت به سطوح سال گذشته بهبود یافت، اگرچه این بهبود در سراسر شهر یکنواخت نیست. مناطق مرکزی شهر و شمال شرقی به سمت شرایط متعادلتر پیش میروند، در حالی که مناطق جنوبی و شمال غربی با حدود ۱.۶ ماه عرضه همچنان با محدودیت عرضه مواجه هستند.

قیمت معیار بدون تعدیل به ۷۶۰,۵۰۰ دلار افزایش یافت، که حدود ۵ درصد بیشتر از فوریه گذشته است. قیمتها در همه مناطق افزایش یافت، با بزرگترین رشد نزدیک به ۸ درصد در منطقه مرکزی شهر.

خانههای نیمهمستقل

در فوریه ۲۴۰ لیستینگ جدید وجود داشت، که ۷ درصد بیشتر از سال ۲۰۲۴ است. فروش با کاهش نزدیک به ۱۴ درصدی نسبت به سال ۲۰۲۴ به ۱۶۵ واحد رسید. این شکاف بین فروش و لیستینگهای جدید، موجودیها را ۴۶ درصد افزایش داد، هرچند همچنان زیر میانگینهای بلندمدت برای این بخش در فوریه باقی مانده است. تنوع زیادی در ماههای عرضه در سراسر شهر وجود داشت، با کمترین میزان فقط یک ماه در منطقه شمال غربی در مقابل بیشترین میزان ۸ ماه در منطقه شرقی.

قیمت معیار بدون تعدیل از سطوح اواخر تابستان و اوایل پاییز فراتر رفت و با افزایش نزدیک به ۷ درصدی نسبت به سال گذشته به ۶۸۳,۵۰۰ دلار رسید. این افزایش با رشد قیمت در همه مناطق پشتیبانی شد، با بزرگترین رشد حدود ۸ درصد در مناطق مرکزی شهر و جنوبی.

خانههای ردیفی

مانند سایر انواع املاک، فروش نسبت به سال گذشته بیش از ۹ درصد کاهش یافت، در حالی که لیستینگهای جدید نزدیک به ۴ درصد افزایش یافت. با وجود کاهش فروش، هر دو فروش و لیستینگهای جدید بالاتر از میانگینهای بلندمدت برای این ماه باقی ماندهاند. این کاهش فروش، موجودیها را به ۶۵۵ واحد رساند که بیش از دو برابر سطح سال گذشته است، هرچند هنوز کمتر از میانگینهای تاریخی فوریه است. ماههای عرضه در سراسر شهر بهبود یافت؛ مناطق جنوبی و شرقی با کمتر از ۱.۵ ماه شرایط محدودتری دارند، در حالی که منطقه شمال شرقی نزدیک به ۳ ماه عرضه دارد.

قیمتهای معیار بدون تعدیل هنوز زیر سطوح پاییز است اما با افزایش نزدیک به ۳ درصدی نسبت به سال گذشته به ۴۴۶,۸۸۰ دلار رسیده است. قیمتها در همه مناطق افزایش یافت، با افزایشهای اندک در مناطق جنوب شرقی و شمالی، در حالی که منطقه شرقی با افزایش قابل توجه ۱۲ درصدی نسبت به سال ۲۰۲۴ مواجه شد.

مانند سایر انواع املاک، فروش نسبت به سال گذشته بیش از ۹ درصد کاهش یافت، در حالی که لیستینگهای جدید نزدیک به ۴ درصد افزایش یافت. با وجود کاهش فروش، هر دو فروش و لیستینگهای جدید بالاتر از میانگینهای بلندمدت برای این ماه باقی ماندهاند. این کاهش فروش، موجودیها را به ۶۵۵ واحد رساند که بیش از دو برابر سطح سال گذشته است، هرچند هنوز کمتر از میانگینهای تاریخی فوریه است. ماههای عرضه در سراسر شهر بهبود یافت؛ مناطق جنوبی و شرقی با کمتر از ۱.۵ ماه شرایط محدودتری دارند، در حالی که منطقه شمال شرقی نزدیک به ۳ ماه عرضه دارد.

قیمتهای معیار بدون تعدیل هنوز زیر سطوح پاییز است اما با افزایش نزدیک به ۳ درصدی نسبت به سال گذشته به ۴۴۶,۸۸۰ دلار رسیده است. قیمتها در همه مناطق افزایش یافت، با افزایشهای اندک در مناطق جنوب شرقی و شمالی، در حالی که منطقه شرقی با افزایش قابل توجه ۱۲ درصدی نسبت به سال ۲۰۲۴ مواجه شد.

آپارتمانهای کاندومینیوم

فروش در فوریه به ۴۷۳ واحد رسید، ۲۶ درصد کمتر از سال گذشته اما همچنان بسیار بالاتر از میانگینهای بلندمدت برای بخش آپارتمانها در فوریه است. تعداد لیستینگهای جدید نسبت به سال گذشته تقریباً ثابت بود، اما با ۸۵۲ واحد، بالاترین میزان ثبتشده برای این ماه بود. به دلیل لیستینگهای جدید رکوردی، موجودی ۹۰ درصد نسبت به سال گذشته افزایش یافت و به سطح نزدیک به رکورد رسید. ماههای عرضه در فوریه به ۳.۱ ماه رسید، که افزایش ۱۵۵ درصدی نسبت به سال ۲۰۲۴ را نشان میدهد اما هنوز بسیار پایینتر از سطوح رکوردی بین سقوط قیمت نفت در سال ۲۰۱۴ و همهگیری است.

قیمت معیار بدون تعدیل برای فوریه ۳۳۴,۲۰۰ دلار بود، که قابل مقایسه با سطوح پاییز و تقریباً ۴ درصد بیشتر از قیمتهای سال گذشته است. بزرگترین رشد قیمت در منطقه غربی با بیش از ۸ درصد رخ داد.

حقایق بازار منطقهای

ایردری

بازار کلی ایردری در فوریه تقریباً با میانگینهای بلندمدت خود همراستا بود، با کاهش فروش در حالی که لیستینگهای جدید و موجودیها به سطوح معمول این ماه افزایش یافت. فروش نزدیک به ۹ درصد کاهش یافت و به ۱۲۳ واحد رسید، در حالی که لیستینگهای جدید با افزایش نزدیک به ۲۳ درصدی به ۲۲۵ واحد رسید. این کاهش فروش همراه با افزایش لیستینگهای جدید، موجودیها را به بیش از دو برابر سال گذشته، یعنی ۳۴۵ خانه، رساند. در نتیجه، ماههای عرضه به نزدیک ۳ ماه افزایش یافت، که با میانگینهای بلندمدت همراستا و بالاترین میزان دیدهشده در این بازار از قبل از همهگیری است.

قیمت معیار بدون تعدیل برای فوریه عملاً نسبت به ماه گذشته ثابت بود و در ۵۳۷,۶۰۰ دلار، زیر سطوح پاییز باقی ماند، اما ۱.۶ درصد بالاتر از فوریه گذشته بود.

کاکرین

فروش در فوریه به ۷۵ واحد رسید، در حالی که لیستینگهای جدید به ۱۲۶ واحد رسید، که هر دو نسبت به این زمان در سال گذشته و بالاتر از میانگینهای بلندمدت بازار افزایش داشتند. موجودی با افزایش بیش از ۴۸ درصدی نسبت به سال گذشته به ۱۹۶ واحد رسید، که بالاترین سطح دیدهشده در هر ماه از بهار ۲۰۲۱ است اما همچنان زیر میانگینهای بلندمدت برای فوریه در بازار کاکرین است. این افزایش موجودی اجازه داد ماههای عرضه به ۲.۶ ماه بهبود یابد، که بالاترین میزان از زمان همهگیری است اما هنوز بسیار پایینتر از سطوح تاریخی این ماه است. شرایط نسبتاً محدود از بازگشت قیمتها به نزدیکی سطوح رکوردی که در تابستان دیده شده بود پشتیبانی کرد، زیرا قیمت معیار بدون تعدیل با افزایش بیش از ۵ درصدی نسبت به سال گذشته به ۵۷۷,۱۰۰ دلار رسید.

اوکوتوکس

فوریه شاهد کاهش ۴ درصدی فروش نسبت به سال گذشته به ۴۵ واحد بود، هرچند با میانگینهای بلندمدت این ماه همراستا باقی ماند. لیستینگهای جدید با افزایش ۷ درصدی نسبت به سال ۲۰۲۴، و در ۶۰ واحد، بسیار پایینتر از سطوح معمول فوریه بود. موجودی به ۶۹ واحد بهبود یافت، ۱۹ درصد بیشتر از سال ۲۰۲۴، اما مانند لیستینگهای جدید، بهطور قابل توجهی پایینتر از سطوح تاریخی این ماه باقی ماند. این سطوح محدود موجودی همچنین ماههای عرضه را بسیار پایینتر از آنچه معمولاً در فوریه دیده میشود، در ۱.۵ ماه نگه داشت. با وجود شرایط محدود، قیمت معیار بدون تعدیل برای این ماه نسبت به ژانویه تقریباً ثابت و کمتر از یک درصد بیشتر از سال ۲۰۲۴ بود.

برای مشاهده بسته کامل آمار ماهانه شهر کلگری اینجا کلیک کنید.

برای مشاهده بسته کامل آمار ماهانه منطقه کلگری اینجا کلیک کنید.

برای مشاهده بسته کامل آمار ماهانه منطقه کلگری اینجا کلیک کنید.

د فبروري په میاشت کې د موجوداتو په کچه کې د پام وړ کلنۍ وده

د موجوداتو کچه د دویمې میاشتې لپاره په پرله پسې توګه د تېر کال په پرتله د پام وړ وده کړې، چې د فبروري په میاشت کې ۷۶ سلنه زیاتوالي سره ۴,۱۴۵ واحدونو ته رسېدلې. په داسې حال کې چې د موجوداتو زیاتوالی د ټولو قیمتي کټګوریو په اوږدو کې لیدل شوی، تر ټولو لوی زیاتوالی د ۵۰۰,۰۰۰ ډالرو څخه کم قیمت لرونکو کورونو کې و، په ځانګړي توګه اپارتمانونه او ردیفي/ټاونهاوس کورونه.دا زیاتوالی د اپارتمانونو او ردیفي/ټاونهاوس کورونو په ارزانه برخو کې د پام وړ ودې له امله رامنځته شوی. د فبروري په میاشت کې د ټولو میاشتو عرضه ۲.۴ وه، چې د تېرې میاشتې په څېر وه خو د تېر کال د همدې وخت په پرتله دوه برابره زیاته ده. د اپارتمان په څېر واحدونه د ۳.۱ میاشتو عرضه سره تر ټولو ښه اکمال شوي پاتې شول.

په فبروري کې ۱,۷۲۱ پلورونه ترسره شول، چې د دې میاشتې لپاره د تاریخي اوسط څخه پورته وو، خو د تېر کال په پرتله ۱۹ سلنه کم او د وبا وروسته دورې د ریکارډ کچې په پرتله خورا ټیټ وو. د فبروري په میاشت کې نوي لیستینګونه ۲,۸۳۰ واحدونو ته رسېدل، چې د دې میاشتې لپاره د تاریخي اوسط سره نږدې برابر وو. د دې میاشتې لپاره د پلورونو او نوو لیستینګونو نسبت ۶۱ سلنه و، چې د تاریخي اوسط څخه لوړ خو د تېرو دریو کلونو په هر یوه کې لیدل شوې کچې څخه ټیټ و.

الن ټیننټ، د CREB® رئیس او اجرایوي مشر وویل: «که څه هم زیاتو خلکو خپل کورونه د پلور لپاره لیست کړل، خو په فبروري ۲۰۲۴ کې د پلورونو په پرتله واقعي پلورونه کم وو. نو، موږ د تېرو دوو یا دریو کلونو د پلورونکو بازار فشار کمېدو شاهد یو. په پایله کې، دا د قیمتونو د زیاتوالي سرعت یو څه ورو کړی، چې دا باید د پیرودونکو لپاره ښه خبر وي.»

په فبروري کې د استوګنې ټول غیر تعدیل شوی معیار قیمت ۵۸۷,۶۰۰ ډالر و، چې د ۲۰۲۴ کال پای په پرتله نسبتاً ثابت او د تېر کال په پرتله شاوخوا یو سلنه لوړ و. د قیمتونو بدلونونه د ښار په اوږدو کې توپیر درلود، چې د ښار مرکزي او شمالي سیمو کې کمښت لیدل شوی، په داسې حال کې چې ختیځې سیمې د درې سلنې څخه زیات د قیمتونو تر ټولو لوی زیاتوالی تجربه کړ.